UPDATE: 50% reduction of the LQ user distribution rate is being proposed until the full set of Liqwid v1 features are released (as opposed to the initial 99% temporary reduction included in the original temp check). This includes having everything live such as Agora on-chain governance proposals, LQ staking, initial user distribution releases, additional markets, and a smoother app user experience.

Once we are “Liqwid v1 complete” the shift to a dynamic emissions schedule where we target an APR of XX% (depending on the level of liquidity would be implemented using the same user distribution system, Minswap has implemented a similar model).

If TVL < 100M → 50% APR

If TVL < 500M → 25% APR

If TVL < 1B → 10% APR

If TVL > 1B → even lower APR

*these % figures are examples and are open to community feedback/updates.

Our core team feels this is a significantly more balanced approach to responding to recent community feedback, decentralizing the protocol ownership to early users, while implementing a sustainable long term LQ user distribution system.

For each of the first two months since the Liqwid protocol’s mainnet launch 207,812.5 LQ have been allocated to suppliers and borrowers. For the entire first month (February) there was a single ADA market, on March 1st the DJED market was launched on mainnet. During this short time Liqwid has grown to become the largest lending and borrowing protocol on Cardano.

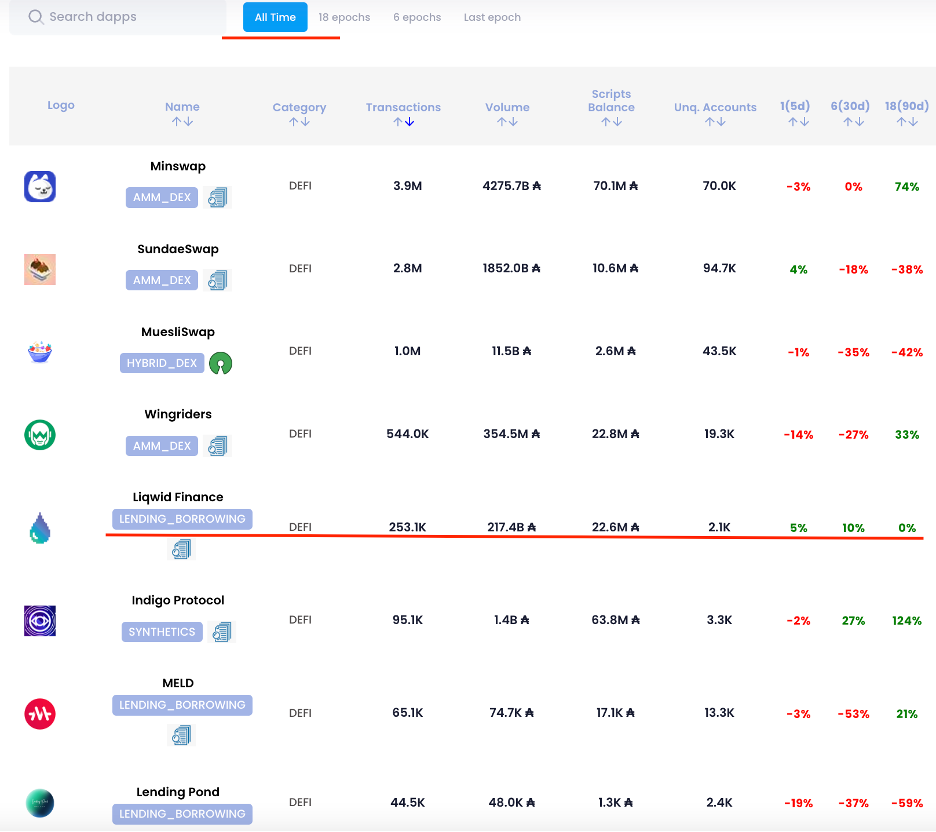

If you compare Liqwid adoption rate to other lending protocols on Cardano that have been live on mainnet for 3-4x longer than Liqwid, the protocol’s usage, volume and adoption rate is incredible. In 2 short months Liqwid has had significantly more volume, TVL and nearly as many individual users as lending protocols live on mainnet for the past 6-8 months. Here is a view of the all-time transaction volume for every DeFi protocol on Cardano (source: https://dappsoncardano.com/).

While some of this early success can be attributed to Liqwid being the first algorithmic liquidity market protocol for pooled lending to launch on Cardano some of it is also due to the LQ User Distribution program, which allocates 47.5% of LQ tokens to users on a 4-year schedule based on their total lending and borrowing volume. The main purpose for the outsized LQ rewards allocation as part of the User Distribution schedule is to decentralize ownership of the Liqwid protocol amongst protocol users.

This is however not the first distribution of LQ with the specific intended purpose of decentralizing protocol ownership: In January 2022 1.5% of the LQ token supply was airdropped to community members in the Liqwid Discord Community server with the stated purpose of decentralizing ownership of the Liqwid protocol to the community. Many of the individuals who received the airdrop were actively involved in protocol and governance discussions for months on end with core team members in Discord and without the possibility of an airdrop having ever been mentioned. There was no prior expectation (as there has been for every single airdrop on Cardano since, mostly as a result of Liqwid being the first Cardano DeFi protocol to successfully complete it and users seeking the “next one”), no ability to game the system for the same reason and unlike ISPOs each user received an equivalent LQ amount irrespective of ADA holdings. In many ways this was the most fair, non-speculative approach to decentralizing ownership of the protocol to community members with the least ability to game the system (again mostly as a result of its simplicity and the fact no warning was given).

Fast forward to now and the LQ User Distribution system which again aims to decentralize Liqwid protocol ownership, now on a much grander scale of nearly half the LQ token supply and we are observing not only contention in the Cardano community over LQ user distribution speeds but also to some degree attempts to game the User Distribution system to maximize LQ rewards via recursive leverage.

As of yesterday, the core team have introduced temperature checks we hope will help to combat the recursive leverage observed in the ADA and DJED markets an important point should be considered: Compound Finance, the protocol which pioneered this form of user distribution (also known as yield farming) faced similar issues in the early days of their COMP distribution program. In some markets analysis shows as much as 80% of borrowed assets in some markets were recursive leverage for the purpose of maximizing COMP rewards.

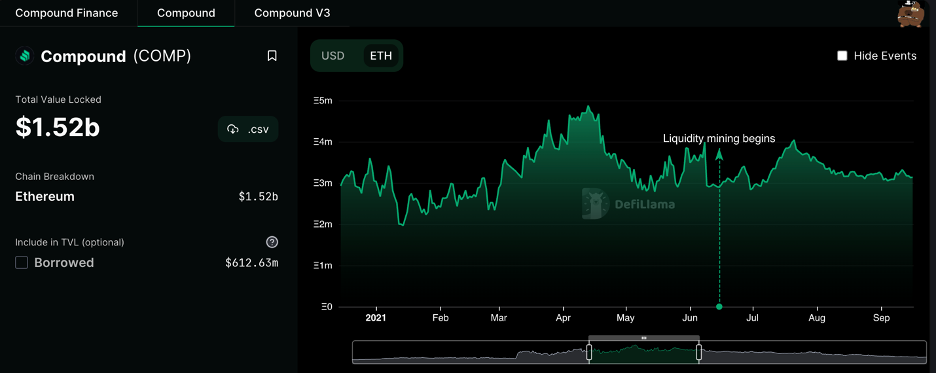

These yield farming driven strategies impose significant liquidity risk to any lending protocol but especially to newly launched protocols with lower levels of liquidity such as Liqwid. It’s important to note that Compound was live since May 2019, at the time COMP distributions began (June 16, 2021) the protocol had grown to ~3M ETH (at the time equal to $7.57B) in TVL (source: https://defillama.com/protocol/compound)

Having the initial 2 years to bootstrap liquidity, launch new products, integrations, deploy new protocol versions and harden the protocol’s infrastructure was pivotal in the success of the COMP distribution program which has successfully decentralized the protocol’s ownership to its users. An interesting point to analyze though, in ETH terms the all time high peak of TVL for the protocol was in April 2021, months before COMP distribution began or was even announced. Also, important to note that 0 COMP was distributed retroactively meaning users who supplied and borrowed ETH and other Ethereum assets on Compound before the June 15th 2021, launch of COMP liquidity mining received no COMP for their lending/borrowing activity.

The data clearly shows that COMP incentives did not boost the protocol TVL and were only successful in their primary stated purpose of decentralizing the ownership of the protocol to its users. Liqwid has faced a lot of negative recent sentiment related to the launch of LQ rewards as part of the User Distribution schedule for the elevated inflation rate and a notion that the protocol’s base utility as the first algorithmic money market on Cardano could not realize the strong early usage it has without the use of LQ rewards. The data clearly shows this line of thinking is incorrect but with increasingly negative sentiment this has led our ore team to reconsider whether the LQ User Distribution is actually the best path forward for decentralizing the protocol’s ownership.

Could other options such: 1. as an increased yield to LQ stakers, 2. a future airdrop of some form or 3. other distribution methods actually be more effective and community aligned methods to decentralize protocol ownership without incurring the negative feedback from the wider Cardano community?

In the case of Compound multiple governance proposals have resulted in a net 80-90%+ reduction in COMP distribution speeds across markets. This began with an experiment to measure how much some % decrease in rewards impacted change in the protocol’s liquidity. This type of experimentation to arrive at 1. a more optimal distribution speed and 2. explore other available options for decentralizing ownership of the protocol proved successful for the Compound community.

The first 2 years of a DeFi protocol’s lifecycle are vital in terms of the strategic decisions protocol teams and communities must navigate to set up for a healthy and successful long-term future. Early Ethereum DeFi protocol’s like Aave and Compound used this time for diligent product developments, integrations and feature rollouts to grow to the TVL sizes we see today.

Liqwid has similar ambitions to grow and scale in TVL as this represents increased utility to significantly more users lending and borrowing Cardano assets. How we get there will be largely driven by our early actions today.

With all of this context now unpacked, let’s return to the main point of this proposal: the distribution rate of LQ rewards to protocol users. The current LQ distribution rates are based on the pre-protocol launch allocation of 47.5%, distributed equally over a 4-year period. After analyzing the ETH TVL data for Compound, reviewing the governance discussions and proposed paths their community took and with responding to community feedback related to the current distribution rate, the core team proposes the following updates:

-

To begin a series of experiments with respect to finding the optimal LQ distribution speed we propose first reducing the LQ distribution rate by 50% and observing the resulting data in terms of protocol liquidity flows. By reducing nearly all LQ incentives to lenders and borrowers we’ll be able to fully analyze the data and observe how the protocol’s liquidity levels react.

-

Working alongside engaged community members, explore alternative options for decentralizing the protocol’s ownership to Liqwid users.

*the LQ distribution rate will remain at the current speed until this proposal vote is complete. This will be one of, if not the very first proposal to complete an on-chain vote in the LiqwidDAO’s Agora instance.

Do you support a reduction in 50% of the LQ user distribution rate until the full set of Liqwid v1 features are released, and at v1 completion implementing a dynamic emissions schedule?

- Yes

- No